We provide information about Financial and Economical aspects of intensive care unit, here.

COSTING MODELS

ICU costing methodology

-

Many attempts have been made to measure the resources used in critical care. However, as noted in a review by Gyldmark, comparisons between studies are difficult, if not impossible, as different studies have included different elements of resource use. ‘Critical to Success’ reported large variations in ICU practice and subsequently costs, questioning the efficiency of ICUs. While this is only a ‘snapshot’ view of critical care, and these data should be interpreted with caution, it demonstrates that resource data collected in a standardised manner is an essential component of modern ICU practice.

-

Two basic methods of costing care were identified from the review, namely the ‘top down’ approach and the ‘bottom up’ approach.

-

Various hybrid costing methodologies have been used in critical care. Defining patients according to a dependency measure (in its simplest form high dependency or intensive care) attempts to overcome the assumption that resources are distributed evenly between patients in the ‘top-down’ approach. A period of ‘bottom-up’ calculation may be used to define the costs of the high dependency patient assuming remaining costs are distributed amongst the intensive care patients.

-

A further refinement is to apportion costs according to dependency using the Therapeutic Intervention Scoring System (TISS. Some studies have found a significant relationship between daily TISS scores and individual patient costs, yet other studies do not support this hypothesis. TISS was originally described as a method for quantifying therapeutic interventions and has been adapted extensively in individual ICUs to reflect local practice. This clearly affects comparison between different ICUs.

The Cost Block Programme

-

The Intensive Care National Working Group on Costing convened between 1994 and 1999 to tackle the methodological problems of undertaking cost comparisons of intensive care provided in different hospitals. For intensive care units (ICUs), a standard method for measuring costs of resources did not exist and this made the evaluation of resource use difficult. The Group was multidisciplinary, comprising professional members from the fields of intensive care, health economics and accountancy and health services research.

-

The Group formulated a list of costing-related questions and sought answers to these questions from a literature review. Having reviewed those papers published between 1974 and 1994, it was apparent that a suitable method, capable of answering more than two of the costing-related questions, did not exist. It was also clear than none of the methods described in the literature could be deemed appropriate for routine use, due to their complexity and resources required for implementation. The Group therefore developed a standard method of costing to overcome this specific problem and others relating to the heterogeneity of accounting practices employed by individual NHS trusts.

-

The ‘top-down’ approach was thought capable of providing data that would answer a number of the questions raised by the Group, because it enabled the identification of the major cost components. However, the ‘top down’ approach would not be useful for providing answers to questions such as ‘how does cost per category of patient vary with throughput?’ or ‘how do we include quality?’. It would have several practical applications. For example, if data were collected annually, it would provide a means for determining average daily costs per patient and the marginal costs of opening an additional ICU bed.

-

The Group developed their own method, starting with the identification of budgetary components associated with resource use in critical care. The selection of the most important components was based on relevance, data availability and ease of collection. The validity of the data was considered. Proportion of cost contributed by each of the components was considered together with whether the costs were incurred by the ICU. This process led to the definition and grouping of components as ‘cost blocks’.

-

The methodology was piloted in eleven ICUs, after which the definitions were refined; a second pilot study was repeated in twenty-one ICUs. The pilot studies revealed that cost blocks 1-3 (Capital Equipment, Estates and Non-Clinical Support Services) accounted for only 15% of the total cost of the ICU and were difficult to collect, inaccurate and not within the control of the ICU.

-

The Intensive Care National Cost Block Programme was launched in November 1999.

How does the cost block method compare to other methods for costing?

-

The cost block method was developed with the principle aim of facilitating meaningful comparisons between individual ICUs. It was intended that the method be suitable for use in any ICU. The cost block method determines the total expenditure of an ICU and apportions this by the throughput of the ICU (number of patients and their length of stay) and organizational capacity (number of beds). In this way, average costs per patient, per patient day and per ICU or HDU bed can be deduced.

-

In nine of the studies reviewed by Gyldmark, it was unclear what cost components were included. Of the remaining eleven studies, four excluded medical and nursing staff costs which represented 53% of total ICU costs in cost block pilot studies. Three of the eleven studies excluded the cost of disposables, and one excluded the cost of drugs and fluids. It was often the case that the inclusion of other cost components within the studies reviewed was assumed rather than known.

-

There are a number of different ways of arriving at individual patient costs. The ‘topdown’ method has the disadvantage of being inaccurate at the individual patient level but is easy to calculate. The ‘bottom-up’ approach is much more time-consuming as resource costs are summated from individual items of care and then ascribed to individual patients. Despite its higher degree of accuracy, it is a difficult method to reproduce in different hospitals.

-

The ‘bottom-up’ method is used to produce a cost per patient day by adding together the patient’s use of individual resources. The cost block method, on the other hand, is unable to measure differences in resource use incurred by individual or groups of patients. In bottom-up costing, each resource is broken down into its smallest unit and multiplied by the number of units used. For example, if a patient requires a nurse for ten minutes then a cost per minute of a nurse’s time is required in order to produce an accurate total cost.

-

Micro-costing or activity-based costing are terms frequently used to describe bottom- up costing principles. Activities of care have been used for costing individual intensive care patients since 1995 at the Royal Hallamshire Hospital, Sheffield. The concept behind the activity-based costing methodology is that the clinical care delivered to patients is partitioned into discrete elements (the activities). The cost of patient care is then determined by allocating resources (and therefore costs) against each activity. The total patient-related cost of care for an individual patient is determined from the sum of the costs of the activities delivered to that patient. The disadvantage of this method of costing is that it requires a Patient Data Management System with a computer terminal at each patient’s bed-side for the nursing and medical staff to record the clinical procedures and interventions performed on each patient. These data are collected prospectively and have to be checked against the medical records for any omissions. Therefore, the commitment of staff working on the ICU is mandatory to ensure accurate recording of data.

Practical implications of the cost block method

-

A number of factors influence the varying degrees of expenditure on intensive care in different hospitals. Technological developments, differences in unit characteristics and differences in methods of costing are thought to be three such factors. Heterogeneous case-mix is another problem. A study of the cost of individual patients admitted to a Canadian ICU found that the 8% of their ICU patients who consumed the highest costs equated to the same amount of resources as the 92% of patients with the lowest costs. The cost block method overcomes the problem associated with different methods of costing, insofar that more accurate study of the costs and consequences of intensive care can prevail. The cost block method takes accounts of the size of the ICU, its geographical location, whether it is located in a university or a nonuniversity hospital and its throughput. The cost comparisons, made possible through a representative sample of ICUs using the cost block method, are very useful to individual hospitals as it allows them, for the first time, to compare their levels of expenditure with other ICUs.

-

Future research correlating standardised mortality ratios (SMRs) to the cost components of the cost block method should supply further knowledge of the resources required to achieve optimal outcomes.

-

The cost block method is being collected in approximately one third of hospitals. The investigation of routinely collected data for its ability to explain observed expenditure variation between individual units has identified throughput to be a key factor.

-

The method has wider implications for the comparison of cost data across Europe. The collection of cost data using a standard method in different European countries would enable inter-country cost comparisons to be made providing adjustments for economic differences between countries were ensured.

FINANCIAL MANAGEMENT SYSTEMS IN THE CRITICAL CARE UNIT

Balancing supply and demand

-

All systems for financial management within the critical care unit have to operate within the resource constraints of the overall structure of the NHS and local health economies. Demand for critical care services continues to increase and is not matched by a commensurate increase in healthcare resources. The reasons for the increase in demand are multifactorial but include:

-

Ageing population

-

Increased public expectation

-

Technological advance

-

Changes in disease demography.

-

-

Strategies for dealing with the imbalance between resource and demand include:

-

Reduction in demand

-

Limitation of supply (rationing)

-

Improved efficiency.

-

-

Implicit rationing is already imposed within the NHS but the degree varies between health authorities and trusts as local priorities determine the proportion of resource allocated to critical care. This is largely a result of the ‘overhead’ approach to funding and the effect of multiple paymasters.

-

Separation of critical care funding from other specialties’ costs and a reduction in the number of paymasters by moving to regional funding could remove some of the inequities of present funding systems.

-

Critical care financial management systems must seek to rationalise expenditure since the only other alternative in a resource limited healthcare system is rationing of the service.

-

All systems have to function within the design of local trust structures. All have the advantage, however, of making explicit the resources available to the unit and, therefore, allowing clinicians and managers the baseline information they need to lead the unit and to make explicit the service targets that they are expected to deliver.

The fixed budget model

-

This model focuses on the use of expenditure budgets as the overall control mechanism (as opposed to a financial reconciliation of income and expenditure budgets).

-

Under this model, all income for the trust is centrally pooled and redistributed to cost centres as an allowance, or expenditure budget. Each cost centre is expected to deliver a service to either patients, usually expressed in activity terms, or (for cost centres such as theatres, radiology, pathology and critical care) to support other departments. Targets are set and must be delivered within the scope of the budget allocated.

-

Some flexibility can be built in at trust budget setting meetings. This forum is an opportunity to negotiate an adjustment to the expenditure budget based on known or projected changes in activity, demand or performance. This would normally occur on an annual basis, with ad-hoc meetings during the year if either the directorate or the trust needed to review financial plans. The release of new sources of funding or new demand expectations – such as those in ‘Comprehensive Critical Care’ – ought to be a catalyst for in year review.

-

The budget for a critical care unit should, as a general principle, reflect the actual make-up of the department. That is to say that each component of the service should be represented on the balance sheet just as it is represented in the actual delivery of service. In a fixed budget, overhead and indirect costs (e.g. cost of main taining buildings, costs of support by other departments) are not attributed to the ICU and are treated as a hospital overhead or as part of another department’s budget. Indeed some direct costs (e.g. sterile supplies, laundry of sheets) are often not attributed to the ICU budget.

-

Within this system, the ICU management team attends a fixed service planning/budget setting meeting. The ICU budget is negotiated in the context of the previous year’s performance and an estimate of ICU activity required to support the trust’s performance targets for the next year.

-

Throughout the year, the ICU performance is monitored against agreed activity, quality and financial targets. Variances are discussed and explained – for example any resulting from an increase in another directorate’s activity. Where expenditure is in excess of budget, the ICU management team would need to negotiate an additional budget allocation. Success is likely to be dependent on whether the trust has obtained additional income for the source of the increased activity.

-

The main advantages and disadvantages of the expenditure budget system in ICUs are summarised below.

-

Advantages:

-

The cost centres negotiate a financial framework in which to deliver services, based on a discussion around demand, activity and other targets.

-

A fixed budget within a financial framework leaves the cost centres with scope to make incremental or small-scale changes.

-

There is relatively little bureaucracy, as there is no cross charging (trading account, internal purchasing). Once the budget is set financial management is focused on containing expenditure.

-

A fixed budget helps to focus attention on trust objectives (rather than individual or directorate agendas).

-

A fixed budget may promote a culture of mutual co-operation between departments.

-

The expenditure-budget system can work extremely well in smaller trusts, where close liaison across cost centres is possible and staff can work together towards common shared goals.

-

-

Disadvantages

-

Without a cross-charging mechanism, there is no strong incentive to ensure accurate and timely activity monitoring across the trust.

-

The ICU is exposed to the risk of increased demand, due to a change in another department’s activity.

-

It can be difficult for cost centres to make significant service changes, or to develop new services, as there is no direct link between externally-negotiated funding and the budget.

-

There is an inbuilt financial disincentive around the care of expensive patients.

-

-

Disadvantages can be overcome. Data accuracy can be assured by a strong culture of clinical audit and quality monitoring. The risk to support departments of an increase in activity in another department can be minimised with close liaison between cost centres.

The trading account model

-

This model recognises that ICU activity is determined by the activity of user departments. A trading account allows the ICU to recoup costs related to patient activity (variable costs) from user departments thus maximising flexibility. User departments gain access to ICU beds that may otherwise be closed to contain expenditure within a fixed budget. A small fixed budget is maintained to cover costs that are not related to patient activity (fixed costs).

-

The central theme of the trading account is the direct relationship between income and expenditure. It seeks to factor in relevant aspects of providing critical care services: availability of staff, resources for equipment, consumables and drugs and the relationship between referring clinicians and the unit.

-

The model attempts to match the flexible use of capacity with a parallel flexibility in funding. For ICUs this principle has the added advantage of minimising the financial risk to the department which does not have control of referred activity. For the trust that risk is taken on board elsewhere, for instance within the budgets of referring departments.

-

Fixed costs of managing the unit remain exactly the same irrespective of the number of beds occupied although extreme changes in activity may require adjustment of the fixed cost budget. Fixed costs include:

-

Staff

-

ICU managerial staff

-

Medical staff

-

Senior nursing staff

-

Administrative support staff

-

Technical support staff

-

-

Equipment

-

Educational staff

-

Research staff

-

Replacement

-

Maintenance

-

-

Generally, the costs of the above categories are determined by the number of beds expected to be available or the predicted activity. In this respect the fixed costs budget is exactly the same of the fixed budget model.

-

Conversely the variable costs are those directly associated with activity. These are the costs that will change as a result of one more or less bed day of activity:

-

Staff

-

Bedside nursing staff

-

-

Supplies

-

Pharmacy

-

Blood and blood products

-

Disposables

-

Sterile supplies

-

Administrative supplies

-

Catering supplies

-

-

Investigation

-

Laboratory

-

Radiology

-

-

Support services

-

Operating theatre

-

Professions allied to medicine

-

Chaplaincy

-

Mortuary services

-

-

The trading account generates an income that is directly related to patient activity and expenditure is managed according to this income.

-

Because the fixed budget devolved to ICU is a fraction of the total expenditure, each user department is given a budget from which they can purchase their ICU service.

-

Advantages

-

Referring departments have a budget for their use of ICU, shifting the financial responsibility for referral to the referrer.

-

The financial risk of longer stay patients or increased activity following, for instance, a new consultant appointment is moved to the source of such activity rather than the ICU.

-

Financial management is focused on balancing income and expenditure rather than simply containing expenditure.

-

In larger trusts where close liaison between cost centres may be difficult interaction is made more explicit. Developments in all interacting cost centres are forced to take account of the implications for ICU.

-

Central to a well-run trading account is accurate and timely activity monitoring. Clearly the overall financial risk to the trust does not disappear but it makes explicit the requirement to think through at a proper strategic level the impact and cost of ICU services.

-

-

Disadvantages

-

Referring departments are exposed to financial risks of increased ICU activity that may not be budgeted. A single long stay patient could wipe out a user’s budget.

-

The matching of ICU availability to demand may be contrary to trust objectives.

-

The need to track activity accurately increases bureaucracy.

-

[1] Referrers may view the ICU as unfairly protected from the need to manage expenditure as income increases with activity.

-

-

Where the ICU accepts direct referrals from outside the trust it can purchase activity from itself against any commissioning model that sets a specialty line for critical care. All users are thus treated equitably.

Managing the budget

-

Although the trading account model allows the critical care unit to increase its income according to demand that leaves a reduction in resource somewhere else in the healthcare system. This may be appropriate if the priorities of the healthcare system can tolerate that reduction and wider use of trading accounts is one way of matching resource consumption to whole system priorities. A simple example may be the choice between two equally effective antibiotics: one is expensive to purchase but does not require laboratory measurement of levels, while the other is cheap but does require laboratory levels. Using the trading account model the first antibiotic may be the best choice.

-

The fixed budget model leaves expenditure control as the only way of managing the budget. If the budget was based on system-wide priorities this would not matter, although there is little scope for accommodation of changing priorities. Furthermore, using the antibiotic example from above most would select the second antibiotic since the costs of the laboratory measurements come out of another department’s budget.

-

It is clear that resource limitation in the healthcare system as a whole must be matched by a reduction in expenditure. This can be achieved by increased efficiency (reduced cost per patient treated) or by reducing demand. For the critical care unit reducing demand is unlikely to be achievable but reducing access has a similar effect on the budget. Increasing efficiency is difficult as technological advance (in this context technology includes pharmaceuticals) will, in the majority of cases, increase costs.

-

Some technological developments may be cost beneficial but the cost is borne by the ICU and the benefit is reaped in another budget. Since there is little scope for horizontal movement of funds in public finance it may be difficult to procure the technology despite its benefit to the healthcare system as a whole. It is hoped that the National Institute for Clinical Excellence will focus on system wide benefits to allow such procurement.

-

Staff costs make up the major part of all critical care expenditure such that the most effective way of reducing expenditure is to reduce staff costs. This approach is often taken when beds are closed to limit access, although it is least effective in small units where a closed bed may not allow a reduction in staff numbers as a higher proportion of the total is considered as a fixed cost.

-

Increased efficiency can be achieved by reducing the average numbers of nurses per patient, recognising that one to one nursing is not a standard in most other Western societies. Alternatively, efficiency in terms of cost per patient may be achieved by reducing the numbers of skilled nurses per patient and replacing them with unskilled (and therefore cheaper) assistants.

-

Non-staff costs may be controlled by formulating agreed policies for admission and treatment taking into account real cost benefits where alternative treatments are associated with differing costs. This approach can most obviously be applied to formularies for drug choice and stock lists for disposables. Use of a high cost technology rather than a cheaper one for an equivalent benefit represents, in economic terms, a lost opportunity.

-

Costs of critical care vary between units and are, in part, dependent on the organization of the unit. An open unit may have little in the way of treatment or admission policies with little control of expenditure. A closed unit will usually have well developed policies and uniformity of treatment leading to better expenditure control.

-

Since the fixed cost element is not related to patient activity a large ICU will have lower average costs than a small ICU. This is because treatment of a larger number of patients means the fixed costs represent a smaller proportion of the total. Thus a larger unit is more efficient than a smaller unit in economic terms. Similarly, the purchase of revenue items (up to £5000 per item allowed in NHS financial rules) in a larger unit will be associated with a lower proportional increment in costs than in a smaller unit.

-

The factors affecting budget management decisions are many and varied. Critical care medicine has struggled to demonstrate its effectiveness and, without doing so, will not achieve adequate funding to meet the demand. Resource movement from other parts of the healthcare system will only become possible where benefits of critical care medicine can be proved worthy of releasing that resource. In the meantime budget management is focused on increasing efficiency. The principles of ‘Comprehensive Critical Care’, particularly relating to outreach care, may help manage demand. Without these principles of rationalisation the reduction of supply (rationing) becomes the only viable method of containing costs within limited resources.

PRICING AND CONTRACTING

Definition of prices

-

The link between costs and prices is fundamental to the contractual process. The ‘NHS Costing for Contracting Manual’ sets principles for NHS pricing.

-

Prices should be based on cost with no intention to make a profit.

-

Prices should be based on a costing process that recovers all costs associated with a given level of activity so that total anticipated costs divided by total anticipated activity gives the unit price.

-

There should be no planned or deliberate cross subsidisation of costs, i.e. prices should not be reduced in one area and subsidised by increases in another.

-

Applied literally this means that all costs are apportioned on a logical basis across all recoverable activities.

-

Costs may be defined as:

-

direct i.e. directly attributable to a contract activity, e.g. critical care nursing

-

indirect i.e. apportionable on the basis of a recognisable activity statistic, e.g. critical care use of physiotherapy

-

overhead i.e. more difficult to apportion and not related to patient activity, e.g. corporate management costs, building maintenance

-

-

An alternative way of analysing costs would be:

-

variable i.e. moving up and down with volumes of activity, e.g. bedside critical care nursing costs. Variable costs will include some direct costs and should include indirect costs as defined above.

-

fixed i.e. not moving with activity, e.g. non-bed side nursing costs, medical staff costs. Fixed costs will include some direct costs and all overhead costs as defined above.

-

-

For any given size of facility and activity categorising costs as in 5.1.6 or 5.1.7 above will produce identical totals. However, where activity changes the latter analysis will reflect the changes more accurately in the contracting process.

Contracts

-

A contract (known as a Service Level Agreement – SLA) generally contains arrangements to vary the amount paid in accordance with the variation of activity from the contract baseline.

-

As an example, lets say a critical care unit was negotiating one contract which had been set at the level of activity that occurred in the previous year, e.g. 1500 bed days. If the unit of activity was priced at £2000 per bed day (the total cost of providing the service) the income from this contract would be £3 million. If the occupancy to provide 1500 bed days was 68% (a six bedded critical care unit) and this occupancy increased to 80% there would be an additional 252 bed days with associated costs. Costs would not however rise at the full rate of £2000 per day since, for instance, building costs and medical costs (fixed costs) would not rise. However, bedside nursing costs and costs of drugs, consumables, blood etc. would all increase. This is generally covered in contracts by having a marginal (variable) cost clause for variations from target activity. For example, if the marginal costs clause was 50% then the hospital would receive £252,000 (252 days x £2000 x 50%) for the additional activity outlined above.

-

In setting a marginal price it should be noted that the variable cost element of additional activity may be higher than the variable cost element used for the contract. Additional nurses, for example, are often sourced from agencies at costs significantly greater than those of permanent staff on the payroll. The contract would need to take account of the short term effect of these additional costs.

-

In practice, for critical care units (which have significant variable costs) identifying the variable costs properly and incorporating clauses in contracts (SLAs) that appropriately reimburse the department (and therefore prevent overspends) is actually much more important than identifying an absolutely accurate baseline price. It is also of fundamental importance that the definition of activity is understood by both the hospital and purchasing agency. This definition should be a suitable proxy for variable costs.

-

Critical care is by its nature transacted both internally and externally. Internal transactions relate to the costs of a department’s use of critical care. This element is usually included in the prices for that department’s activities. Depending on the budget model (section 4) used in the hospital this element may be recharged to the user department with a trading account or apportioned to the critical care budget.

-

External transactions are generally taken to mean costs associated with patients who are transferred from another hospital and return back to that hospital after treatment. These are identified as critical care activity in SLAs and the currency of the transaction is usually bed days or patient dependency scored bed days.

-

It is important to recognise the cost differentials that exist between the two types of workload. External referrals are often more complex and, therefore, more expensive than internal referrals. There are also fewer of them. The marginal costs charged on to purchasers should recognise the difference between the two types of activity to ensure purchasers pay appropriately and avoid over-charging.

Specialist commissioning and Critical Care Networks

-

The above has been written assuming that critical care is supplied as a service within the normal contractual (SLA) arrangements, probably to several or many purchasing agencies. At the time of writing, a debate is taking place as to whether these arrangements should be totally or partially changed so that one purchasing agency would take lead responsibility for purchasing critical care services over a wider area or region. Such an arrangement is called specialist commissioning and is considered appropriate where:

-

services are specialised and need to be carried out in a small number of units

-

services would benefit from a planned approach (either relating to rationalization or expansion)

-

small numbers of expensive referrals would benefit from a shared ‘risk pool’ of purchaser funding (similar to an insurance policy approach)

-

-

All three of these criteria apply in some respect to critical care services and, in particular, to those transfers made between hospitals for more specialised care.

-

The merger of health authorities into strategic agencies with purchasing managed by small primary care groups may prove to be a driver for specialist commissioning of critical care.

-

Though the debate over how specialised commissioning will affect critical care continues, what is already clear is that its implementation will lead to a need for more sophisticated activity reporting and with it an even more transparent view of how costs vary with each activity.

-

Running alongside specialist commissioning is the development of local Critical Care Networks. These have developed out of the NHS modernisation plan and the view that collaboration and mutual support between hospitals can reduce the effect that individual hospitals suffer as a result of peaks and troughs of activity. The networks also allow for co-operation on shared protocols, education and other common issues.

-

It is probable that these networks will eventually grow to have a role in the contracting process. One view of the way contracting might work in the future is that a lead purchasing agency works with a Critical Care Network to purchase all the critical care activities within their local area.

CAPITAL ASSETS, EXPENDITURE AND ASSET ACCOUNTING

Capital assets and capital charges

-

The ‘NHS Trust Capital Accounting Manual’ defines a capital asset as a tangible productive resource with an expected life in excess of one year. Capital assets usually require repair and maintenance and have a cost of £5000 or more (including VAT).

-

Since its inception, the NHS has always received a separate funding stream for the purchase of assets. Until 1991 no revenue charges arose from assets purchased from capital funding, but from April 1991 revenue charging, reflecting use of capital assets, was introduced. These capital charges were designed to:

-

Increase awareness of the costs of using assets and provide incentives to use them efficiently

-

Ensure the costs of asset use were included in the calculation of contract prices

-

Promote the forward planning of asset replacement.

-

-

Capital charges are relevant to all assets owned by NHS trusts except those that are either donated or have a zero (written down) book value. Assets typically are either land, buildings or equipment.

-

Assets are brought into the balance sheet at their purchase cost which is subsequently revalued as a result of either periodic assessment (land and buildings) or annual indexation (equipment).

-

Each asset is given an asset life and a calculation is made which results in a charge to the trust’s revenue account. For example, a ventilator costing £20,000 with a ten year life would be written down to a zero book value by 10 revenue account charges of £2000 over a 10 year period (assuming zero inflation). This charge to revenue is termed depreciation. All assets are depreciated in this way except land which is assumed to retain its value through time.

-

As the trust has to take account of all of its costs in contracting, the depreciation charge to revenue forms part of the calculation of prices used in SLAs. In turn this leads to income which is greater than expenditure and, theoretically, provides funds for future replacement purchases. This cash surplus, together with any received through an External Financing Limit (EFL – effectively an overdraft facility) allows the trust to formulate and deliver an annual capital spending plan (Programme).

-

The key word above is theoretically. Theoretically there should be enough money to replace equipment (through depreciation) and buy new equipment (through the EFL). However, a number of factors tend to prevent this being the case. These are:

-

Revenue overspends eating into cash reserves

-

New developments exceeding the EFL allowance

-

Replacement equipment costing more than old equipment.

-

-

This often leads to a bidding process followed by a prioritisation of bids against available funds. Often replacement equipment gets squeezed out leaving departments to manage as best they can.

Alternative funding of capital equipment

-

There are three alternative routes to increase the availability of funding for capital purchases.

-

Increasing the EFL (or other earmarked funds) through a successful business plan application

-

Bids against trust funds

-

Increasing the External Finance Limit

-

A bid to increase available EFL will need to be made with trust board approval and would usually involve a large sum of money – usually several hundred thousand pounds. The proposal would need to be of strategic significance and be subject to a business plan set out in a prescribed format following a detailed set of rules. So far as critical care is concerned this would only really be relevant where a new unit was being created or an old one completely refurbished.

-

Increasingly bids are now possible against funding earmarked by the Department of Health or regional offices for critical care.

Trust funds

-

Where hospitals have trust funds then equipment purchases may be possible from them. Each hospital will have its own arrangement. Funds are often left to critical care by grateful relatives and these are often restricted in use to improving the critical care environment.

Leasing

-

The third alternative is increasingly common although leasing is usually a last resort and offers less good value than straight purchase. Leasing is a way of financing a purchase without using scarce capital funds, but from an accounting point of view it needs to be considered carefully. This is because accounting rules and the instruments of their compliance (the auditors) distinguish between two types of lease: the finance lease and the operational lease.

-

The finance lease is regarded as a simple finance arrangement entered into in order to get something you otherwise would not be able to afford. In such an arrangement leasing charges are typically the total purchase costs plus finance charge with the ownership passing to the leasee from the leasor after the final payment has been made. From the auditor’s point of view such transactions are treated as capital purchases and are, therefore, charges against the EFL. They have to be accounted for as though they were purchased from capital funds. They, therefore, offer no advantage to the trust and should be avoided.

-

An operational lease should be seen as a type of rental agreement. Key features of an operational lease are that ownership does not automatically pass to the leasee at the end of the lease. It is also required that the total paid over the life of the lease (after deducting sums for inflation and for the inherent finance charge) does not exceed 90% of the original purchase price. This is known as the 90% rule.

-

In practice leasing companies and equipment suppliers seem very happy to offer compliant deals. However, it should be noted that there are two transactions from a procurement point of view: the purchase of the equipment (tender 1) and the choice of the best value lease (tender 2). Equipment suppliers often do not provide the most competitive prices for lease tenders. Advertisements for tender 1 should always include wording to make it clear that the intended purchase will be subject to an operational lease. Generally speaking, for best value to be obtained, a lease with the longest period that is also consistent with the 90% rule is most competitive. The life of a lease should reflect the expected life of the equipment, which is often nearer ten years than five, and leasing quotes should be obtained for a number of lease periods, e.g. five, seven and nine years. As specification and evaluation of leases is a technical area many trusts have employed specialist advisors to obtain best value and these advisors often identify options that are worth considering.

-

Because it is like a rental agreement an operational lease payment is charged in full directly to the revenue account. Any lease deal needs provision to have been made in the revenue budget. Rolling forward equipment provision from lease to lease is, therefore, a lot less difficult than obtaining new equipment where the costs of the lease need to be provided in full. However, before re-leasing replacement equipment consideration should always be given to purchasing (or renting for an extended period) the old equipment from the leasing company. It may, after all, not need replacing!

Ref: Framework for financial management in intensive care, The Intensive Care Society

Intensive care is an integral but expensive component of healthcare in developed countries. An estimate in the US is that fully 2% of the population receives intensive care every year, and overall the percentage of patients who receive intensive care before they die is increasing. Projections of the need for mechanical ventilation predict an exponential growth in the coming years due to the aging population and their over-representation among mechanically ventilated cohorts; this increase in need for mechanical ventilation will be associated with increasing costs of intensive care. Much of the focus of intensive care is on improvements in technology for organ support and resuscitation. Yet quality healthcare also involves appropriate organization of resources, with the potential to both impact patient outcomes and the costs of the care provided. These economic considerations are likely to become increasingly important as the demand for critical care increases in the face of limited resources.

The economics of organizing the delivery of intensive care can focus on the management of human resources and operating costs within an ICU itself, or the use of ICU resources within a healthcare system. This article will focus on both these perspectives, emphasizing issues related to optimal staffing and the economic consequences of different staffing choices.

Perspective regarding costs—The costs of providing critical care can be considered in short-term and long-term time horizons and are incurred to varying degrees by patients, hospitals, insurance companies, the government or other payer, and society as a whole. Thus, the first question to ask when evaluating the economic impact of any organizational change affecting the ICU is which party actually accrues a cost change. In this article, we will primarily focus on the potential economic implications of organization and management choices from the perspective of the individual hospital.

Fixed versus variable costs in the ICU—Hospital costs are comprised of fixed and variable costs. In brief, the fixed costs remain constant and are independent of small changes in the number of patients being cared for in the hospital. They also generally reflect the operational costs required to provide care. Examples of fixed costs in the ICU include staff salaries, the money paid to purchase mechanical ventilators, and the maintenance required on the building. Variable costs are the hospital costs associated with the care of individual patients, and will fluctuate with patient volumes. Examples of variable costs are the costs of specific medications the patient receives or the cost of an additional central venous catheter inserted. The majority of costs associated with care in the hospital are fixed costs, often estimated to account for over 80% of total costs. Whether or not hospital (or ICU) beds are occupied, the hospital continues to pay the fixed costs of care, and therefore most cost reductions associated with any system change will be small if due to changes in variable costs only.

The economics of intensive care from the perspective of the hospital also depend on how a hospital is reimbursed by a health system. For example, under one type of payment system, a hospital receives a set amount of money for the care of all patients, regardless of the number that are actually admitted. Another option is a fixed level of reimbursement to the hospital to provide care for each patient admitted with a specific diagnosis or surgical procedure. In these situations, the actual components of treatment that are provided to an individual patient are not reimbursed separately, but instead the hospital receives a lump sum based upon expected costs. In a “per diem” model, the hospital is paid an additional sum for each day that a patient remains hospitalized. Hospitals can also be paid using a feefor-service model, receiving a sum of money for each additional test, procedure, medication, etc. that is provided to each patient. Within each of these payment schemes, there are opportunities for the hospital to change the system to maximize revenue. In this article, we primarily consider the actual costs of providing treatment when discussing strategies for reducing total costs, rather than strategies to improve the economic outlook for the hospital based on different payment schemes.

Costs within the ICU

Decreasing Length of Stay—Many studies in critical care target reductions in ICU length of stay and equate this outcome with a “cost savings”. In reality, large cost savings will only be realized if the reductions in ICU length of stay result in a reduced number of total admissions and consequent reductions in number of ICU beds and fixed costs of care. In addition, one must cognizant of the concept of “cost-shifting”, in which reductions in costs in one area are accompanied by rises in costs elsewhere in order to address clinical needs. In most situations the actual cost savings associated with decreased ICU length of stay therefore comprise only a small fraction of total costs. For example, Kahn and colleagues analyzed the potential cost savings attributable to reductions in ICU length of stay for ICU survivors who had received mechanical ventilation and ICU admission of more than three days. The authors found that the mean variable costs of the last day in the ICU was $397, while the cost of the next day on the hospital ward was $279; thus, reducing ICU length of stay by one day would only result in a cost savings of 0.2% of all hospital expenditure. Conversely, if there is typically high demand for ICU resources (and the absolute number of patients in the ICU remains relatively constant), reducing ICU length of stay can paradoxically increase variable costs because higher acuity patients requiring more intensive and expensive treatments replace the lower-acuity patients who are discharged. Moreover, the overall economic effect of accommodating an additional ICU patient may be different depending on the type of ICU and the type of patient. For example, if any decrease in one patient’s ICU length of stay helps avoid the cancellation of an elective surgery such as coronary artery bypass grafting for another patient, the actual economic impact on the hospital may be different than providing admission for an additional patient with pneumonia, but will also depend on how the hospital is reimbursed, as described earlier. In this article we address specific organizational aspects of the ICU by focusing on the actual costs incurred by providing direct care and, where possible, avoid inferences based on economic implications of reducing ICU length of stay. However, we generally consider interventions that decrease ICU length of stay to be desirable.

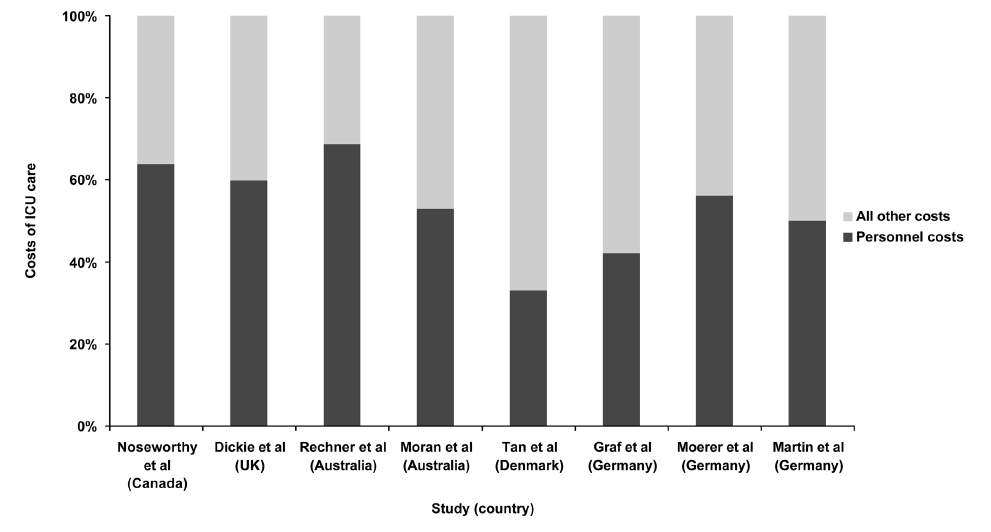

Staffing—The largest and primarily fixed costs of operating an ICU are staff salaries, which are estimated to account for over 50% of fixed costs for all hospitalized patients in the US and 33% to 69% of total ICU costs in other countries (Fig 1). Staffing patterns in the ICU vary markedly between ICUs and between health systems, with variations in the specialty of the physicians, nurse to patient ratios, and the presence of other healthcare professionals on the team. Yet, the large proportion of costs in the ICU taken up by the compensation for its staffseems to be relatively consistent across many countries, despite the different staffing patterns and healthcare systems.

Figure 1.

Estimates of personnel costs associated with the ICU

Nursing—Nurses are an integral, if not the most vital, component of all ICU teams, but perhaps paradoxically, nurse-to-patient staffing ratios and other issues related to the provision of ICU nursing care differ from country to country, from region to region, and even may differ between ICUs in a particular hospital. One European study, for example, from the 1990s found that the majority of ICU nurses cared for two patients, but also observed substantial variation between the planned nurse to patient ratios and actual staffing ratios in the ICU. Studies conducted outside of the ICU have shown that higher nurse to patient ratios and more highly trained nursing staff are associated with fewer adverse events and possibly decreased hospital mortality. Fewer data are available to inform the most cost effective nurse-to-patient ratio in an ICU, although some studies have suggested that higher nursing ratios decrease adverse event rates and lead to better patient outcomes. Obviously, maintaining a higher nurse to patient ratio increases the fixed costs of intensive care and is a major barrier to providing one-on-one nursing in most ICUs (Table 1). It is also possible that savings assocaited with reductions in adverse events for patients could offset the higher fixed costs with higher nursing ratios, but this possibility remains speculative. Some ICUs have adopted a “flex” system that flexibly schedules nurses based on the anticipated workload in the unit at that time, rather than staffing based on the number of admitted patients. This structure may be financially beneficial for the hospital and may also improve nursing satisfaction by matching staff to workload demands. However, this model may also result in unpredictable working hours and salaries for individual nurses.

Table 1

Examples of potential effects on hospital costs of different changes to ICU organization and management

Organizational change |

Possible clinical outcome |

Fixed costs |

Variable costs |

Closing ICU beds |

Unclear |

Decreased |

Decreased |

Intensivist staffing |

Decreased mortality |

Increased |

Unclear |

Pharmacist staffing |

Fewer adverse drug events, deceased LOS |

Increased |

Decreased |

Lower nurse to patient ratio |

Fewer adverse events, decreased LOS |

Increased |

Unclear |

Checklist prompter |

Decreased mortality, decreased LOS |

Increased |

Decreased |

Intensivist Staffing—A great deal of attention is focused on the role of intensivists in the management of critically ill patients, particularly in the United States where there is a mix of staffing systems with only approximately one-third of ICUs covered by intensivists. Overall, most studies demonstrate that intensivist staffing in the ICU improves clinical outcomes and both the American College of Critical Care and the Society of Critical Care Medicine recommend intensivist coverage. However, these studies have varied in the definition of a “closed” or “open” ICU and the number of hours of intensivist coverage, and are hampered by potential selection biases associated with which patients received intensivist coverage as well as other factors such as the type of ICU, concomitant staffing patterns, and ICU culture. Few studies have considered the cost-effectiveness of intensivist staffing. One simulation of intensivist implementation demonstrated cost savings (for the hospital), depending on the size of the ICU, but involved many large assumptions to draw conclusions regarding the impact of intensivists on the hospital system as a whole.

Recent discussions have questioned whether 24 hour in-house intensivist coverage might lead to additional improvements in patient outcomes compared to daytime-only intensivist coverage. One study demonstrated improved compliance with recommended processes of care, but no effect on hospital mortality with 24 hour in-house coverage. Recent work by Banerjee et al examined 24-hour in-house intensivist coverage (versus daytime only) and demonstrated a decreased length of stay for the sickest patients admitted at night and cost savings associated with the decreased length of stay. The study did include estimates of the costs of additional intensivists, but it did not clearly differentiate between fixed and marginal costs of care. Thus it may have potentially over-estimated the costsavings associated with the decreased length of stay.

Multidisciplinary teams—Non-physician team members have a large role in the ICU. Data suggest that multidisciplinary teams on rounds can potentially impact the mortality and length of stay of patients in the ICU. However, expanding the membership of the multidisciplinary team, especially non-nursing healthcare workers, may also increase fixed costs in an ICU (Table 1).

Pharmacists have become an integral component of many ICU teams and several studies demonstrate the economic impact of clinical pharmacists in the ICU. One study in particular detailed the changes made in medication management with the input of a clinical pharmacist over a three month period, with a substantial portion of the consultations (47.1%) resulting in decreased drug costs. More recent studies have examined the impact of clinical pharmacists on management of particular groups of patients, such as critically ill patients with thrombo-embolic or infarction related events and infections. Both studies demonstrated that direct involvement of pharmacists in care led to decreased charges for medications. However, it is important to note that the decreased variable costs may be offset by the fixed costs of the additional salaries.

Perhaps the more important benefit of pharmacists is the potential to decrease adverse drug events. Preventable adverse drug events in the ICU may occur twice as frequently as on the regular hospital ward, primarily due to the greater number of drugs ordered in the ICU, thus making the ICU a prime target for improvement in this area. One study demonstrated a decrease in prescribing errors by two-thirds with the addition of a senior pharmacist on rounds in the ICU. The cost-effectiveness of pharmacists should therefore consider not only the pharmacist’s salary and prescribing costs, but also the potential reduction in the incidence of expensive complications.

Respiratory therapists are common in North American ICUs and often assume important clinical roles, especially with respect to ventilator management. The use of respiratory therapists varies in other countries. Outside of the ICU respiratory therapist-initiated treatment protocols have led to better compliance with institutional algorithms for care. In the ICU, respiratory therapists have been shown to improve compliance with weaning protocols and decreased duration of mechanical ventilation. Guidelines for Weaning and Discontinuing Ventilatory Support recommend that protocols designed for nonphysician health-care professionals should be developed and implemented by ICUs. However, the impact of respiratory therapists on both patient mortality and the economics of care is still not well defined.

The role of the physical therapist in the ICU appears to be evolving to include early rehabilitation, including mobilization of mechanically ventilated patients. Several recent studies have suggested that early rehabilitation may leads to improved patient outcomes, including functional status and length of stay. The full economic impact along with the cost-effectiveness of this intervention requires further study, but limited evidence suggests that this therapy may not lead to increase costs of care, even after accounting for the salaries of the physical therapy team. Further research to evaluate the impact of this intervention is required, but the potential for large system-wide savings may also exist if some of these patients no longer require additional care in nursing or rehabilitation facilities due to early intervention.

Finally, the role of a palliative care team in the ICU, either as a separate consult team or as part of the ICU team itself is still being defined, and the potential financial implications are not yet well explored. No studies have specifically addressed the financial impact of palliative care in patients in the ICU, but introducing these teams may lead to less use of intensive care (in subsets of patients) and reductions in ICU length of stay. However, the cost savings of these interventions may be limited since these patients represent a relatively small proportion of patients who (may) be cared for in the ICU and are likely to influence only the marginal costs of care. It remains unknown whether reducing use of ICU at the end of life through aggressive palliative care can lead to any substantial impact on costs of care.

Standardization of care—Health technology in the ICU, such as mechanical ventilators, pulmonary artery catheters, and other monitoring devices, may represent either fixed or variable costs. Many of these ICU technologies have a limited evidence base supporting their use, and could be considered targets for cost-reduction strategies. The use of intensive care technology has been shown to vary widely among different intensivists working in the same ICU, with no discernible variation in patient outcomes. In one study, the daily discretionary costs of care varied by 43% across different intensivists, with a mean difference of $1,003 per admission and no differences in ICU length of stay or hospital mortality. Reducing use of technology and equipment that have not been linked to improved patient outcomes will likely decrease costs, but can be slow to occur if clinicians consider these to be an integral part of ICU care. A recent example of changing practice is the use of pulmonary artery catheters; after multiple studies failed to demonstrate any clinical benefit associated with their systematic use in different ICU populations, the frequency of insertion has dropped dramatically in the United States.

Standardization of treatment approaches and the use of protocols to help organize ICU care can help reduce the use of unproven and expensive treatments (or at least ensure that they are used only in situations that are supported by strong levels of evidence) and also may lead to increased use of evidence-based therapies and improved patient outcomes. There are many ways to approach standardization of care which include the addition of multidisciplinary staff (as described above), the implementation of checklists, prompting and the use of clinical reminders, and the adoption of clinical protocols and treatment “bundles”. Some of these options have been examined as individual components (such as checklists) and others as “bundles” of care to be delivered together. The combination of checklists on rounds with a “prompter” to ensure that the elements of the checklist were addressed was associated in one single-center study with a decreases in mortality and length of ICU stay, potentially decreasing variable costs associated with care. However, the fixed costs of requiring additional staff to act as “prompter” may offset the potential economic benefit of this intervention (see Table 1).

Many ICUs and hospitals have implemented protocols to limit the use of expensive technologies and treatments to their appropriate and evidence based indications as a strategy to reduce costs and “indication creep”. For example, there has been a substantial increase in off-label use of Recombinant Factor VIIa, with little evidence to support its administration in many cases. In the ICU, even a test as basic as an arterial blood gas may be subject to overuse, with one study demonstrating a substantial decrease in the number of arterial blood gas requests with implementation of guidelines and feedback.

Costs within the healthcare system

Organization of admission and discharge practices and alternatives to care— Since ICU care is almost always more expensive than the care provided on a general ward, choosing to not admit a patient to the ICU will likely decrease the costs of care for that individual. However, such decisions will also likely lead to worse outcomes if appropriate and potentially life-saving treatments are withheld; decreasing the use of intensive care is therefore only a feasible approach to decreasing costs if the admission to the ICU is not appropriate. One study examined the factors associated with being a “high performance” ICU (defined as having a standardized mortality ratio of 1.0 or less) and found that these high performing units all had ICU directors (or a designee) who were authorized to refuse admission to patients not meeting appropriate criteria and to triage requested admissions to extended-stay recovery rooms and intermediate care areas. Cost savings for the hospital may also be realized if sub-acutely or chronically critically ill patients are discharged more expeditiously from the ICU. Although as noted earlier, decreasing ICU length of stay by small amounts (such as a single day) may do little to impact costs of care. However, patients with ongoing respiratory failure traditionally have had few options for care once their needs for acute intensive care are over, yet often stay in an ICU for extended periods. Different institutions attempt to accommodate these patients outside the traditional ICU setting in different manners. The designation of a flexibly sized section of the surgical ICU for the “subacutely ill” allowed for reductions in costly resources (e.g., nursing) without the additional cost of building a separate step-down facility. Similarly, several studies demonstrate that the creation of a physically separate step-down unit may result in reduced costs of care. Another option in some hospitals, particularly in the United States, is to transfer patients quickly out of the acute hospital to receive prolonged care elsewhere. The use of long-term acute care facilities (which can care for mechanically ventilated patients) in the United States has increased dramatically over the past decade. Whether the movement of patients to these facilities is cost effective for the healthcare system as a whole is unclear, but there may be a substantial decrease in costs for the acute care hospital if patients are discharged much earlier.

Regionalization—A broader approach to triage of patients to the most appropriate setting is regionalization of ICU beds and care of ICU patients, particularly mechanically ventilated patients. In the United States this idea has been proposed based on data suggesting that outcomes may be improved for mechanically ventilated patients cared for at higher volume hospitals. Regionalized systems exist for both trauma and neonatal care, and some regionalization occurs in most countries, either through formal systems, or informal networks. However, the barriers to complete regionalization of intensive care are substantial, including concerns regarding strain on patients’ families, lack of strong central authority to organize triage, and the potential to overwhelm capacity at larger hospitals. The impact of regionalization of intensive care for the economics of hospitals is also uncertain, with concern that smaller hospitals may be hurt financially, while larger hospitals receiving patients may not have enough resources.

Alternatively, telemedicine could allow for an increased reach of critical care expertise in remote ICUs by providing access to intensivists. These physicians may offer either monitoring or consultation as needed, and theoretically provide the associated benefits for patient care seen in studies of intensivist staffing. However, the results are inconsistent; two multi-center studies were unable to demonstrate an association between the use of telemedicine and patient outcomes, while one has shown improvements for patients, and a fourth demonstrated some economic benefit.

Assessing the potential impact of telemedicine programs is hampered by the fact that their adoption has often been studied in ICUs that already have high staffing ratios. The true benefit may be found only in small hospitals with limited access to intensivist care. Telemedicine could also be used as a tool to improve the implementation of specific interventions, and to facilitate adherence to current best practice, such as lung protective ventilation or early-goal directed therapy.

Conclusion—The ICU is a complex system and the economic implications of altering care patterns in the ICU can be difficult to unravel. While the clinical impact of many aspects of organization and management have been studied in the ICU, few studies have specifically examined the economics of implementing organizational and management changes. Even fewer have acknowledged the many competing economic interests of patient, hospital, payer and society. It does appear, however, that for certain aspects of ICU organization (e.g., the inclusion of a staff pharmacist on a multidisciplinary ICU team) there may be an alignment of clinical and financial goals for all parties. With continuously increasing healthcare costs there is a great need for more studies focused on economics to inform the optimal organization of the ICU. Ideally these studies should not focus solely on reductions in ICU length of stay, but should strive to measure the true costs of care within a given healthcare system.

Ref: Wunsch H, Gershengorn H, Scales DC, Economics of ICU organization and management, Crit Care Clin. 2012 Jan;28(1):25-37